Turning 30 often brings new responsibilities, career growth, and financial goals. It’s a decade where you begin to realize that building wealth isn’t just about earning more — it’s about managing money wisely. Developing smart financial habits in your 30s can set the foundation for lifelong stability and independence. Here are the best money habits to adopt in your 30s to ensure long-term wealth.

Understand Your Financial Goals

The first step toward long-term wealth is clarity. In your 30s, you’re likely balancing multiple priorities — maybe saving for a home, raising a family, or planning for early retirement. Take time to define your short-term and long-term goals.

Create a simple plan that includes:

- What you want to achieve (like owning a house or becoming debt-free)

- When you want to achieve it

- How much money you need for it

Once your goals are clear, you can align your spending and saving habits accordingly.

Build a Realistic Budget

Budgeting isn’t about restriction — it’s about control. A realistic budget helps you see where your money goes each month. Track your income, expenses, and savings using apps like Mint, YNAB, or even a simple spreadsheet.

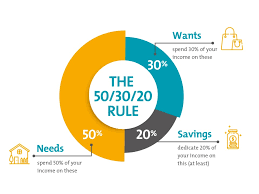

The 50/30/20 rule is a great starting point:

- 50% of income for essentials (rent, food, bills)

- 30% for wants (entertainment, shopping)

- 20% for savings and debt payments

Following a budget helps you live within your means and save consistently, even if your income fluctuates.

Pay Off High-Interest Debt

Your 30s are the perfect time to become debt-free. Credit card balances and personal loans with high interest rates can drain your finances and delay wealth-building. Focus on paying off these debts first using the avalanche method (paying high-interest debts first) or the snowball method (clearing smaller debts for motivation).

Once you’re debt-free, you’ll have more room to save and invest.

Build an Emergency Fund

Life is unpredictable — medical bills, car repairs, or job loss can happen anytime. Having an emergency fund ensures that you don’t rely on loans or credit cards during tough times.

Aim to save at least 3 to 6 months of living expenses in a separate account. Treat this fund as a financial safety net that gives you peace of mind.

Start Investing Early

Investing in your 30s gives you a major advantage: time. Compound interest allows your money to grow exponentially over years. Even small investments can turn into large sums if started early.

Consider diversifying your portfolio with:

- Stocks and ETFs for long-term growth

- Mutual funds for moderate risk

- Real estate for passive income

- Retirement accounts like 401(k) or IRA if you’re in the U.S.

The key is consistency — invest regularly, even if the amount seems small.

Save for Retirement

Retirement might seem far away, but your 30s are the most crucial time to plan for it. The earlier you start saving, the less you’ll need to contribute later. Take advantage of employer-sponsored retirement plans and match programs if available.

If you’re self-employed, open a retirement savings account and make automatic monthly contributions. Over time, these small amounts will grow significantly through compounding.

Build Multiple Income Streams

Relying on one source of income can be risky. In your 30s, explore ways to diversify your income. Side hustles, freelance work, online businesses, or passive income sources like dividends and rental properties can boost your financial security.

Multiple income streams not only increase your wealth but also protect you against unexpected job loss or economic changes.

Track and Improve Your Credit Score

A good credit score affects everything — from getting better loan rates to renting an apartment. Check your credit report regularly and pay your bills on time. Keep your credit utilization below 30% and avoid unnecessary loans.

Improving your credit score can save you thousands in interest over time.

Spend Mindfully

Financial success isn’t just about earning — it’s about spending wisely. Before every major purchase, ask yourself whether it aligns with your goals. Avoid lifestyle inflation — the tendency to spend more as you earn more.

Small changes like cooking at home, canceling unused subscriptions, or buying quality items that last longer can make a big difference in savings.

Protect Your Wealth with Insurance

As your responsibilities grow, protecting your assets becomes essential. Ensure you have the right insurance policies — health, life, home, and auto insurance — to safeguard your finances.

Insurance might feel like an expense, but it’s actually an investment that protects your financial future.

Keep Learning About Money

Financial literacy is an ongoing process. Read finance books, listen to podcasts, or follow experts who share money management insights. The more you understand how money works, the better decisions you’ll make.

Knowledge empowers you to spot investment opportunities, avoid scams, and manage risks effectively.

Plan for Big Life Goals

Your 30s are often filled with major milestones — buying a house, having children, or starting a business. Planning ahead for these big expenses helps you stay financially stable. Create sinking funds for specific goals so that you’re ready when the time comes.

Final Thoughts

Your 30s are not just about earning — they’re about setting the stage for lifelong financial freedom. By adopting smart money habits like budgeting, saving, investing, and spending wisely, you can build a foundation for lasting wealth.

Wealth doesn’t come from one big decision; it grows through consistent, disciplined actions over time. Start today — your future self will thank you.

Leave a Reply